VAT

UK VAT Calculator (Standard, Reduced & Flat Rate).

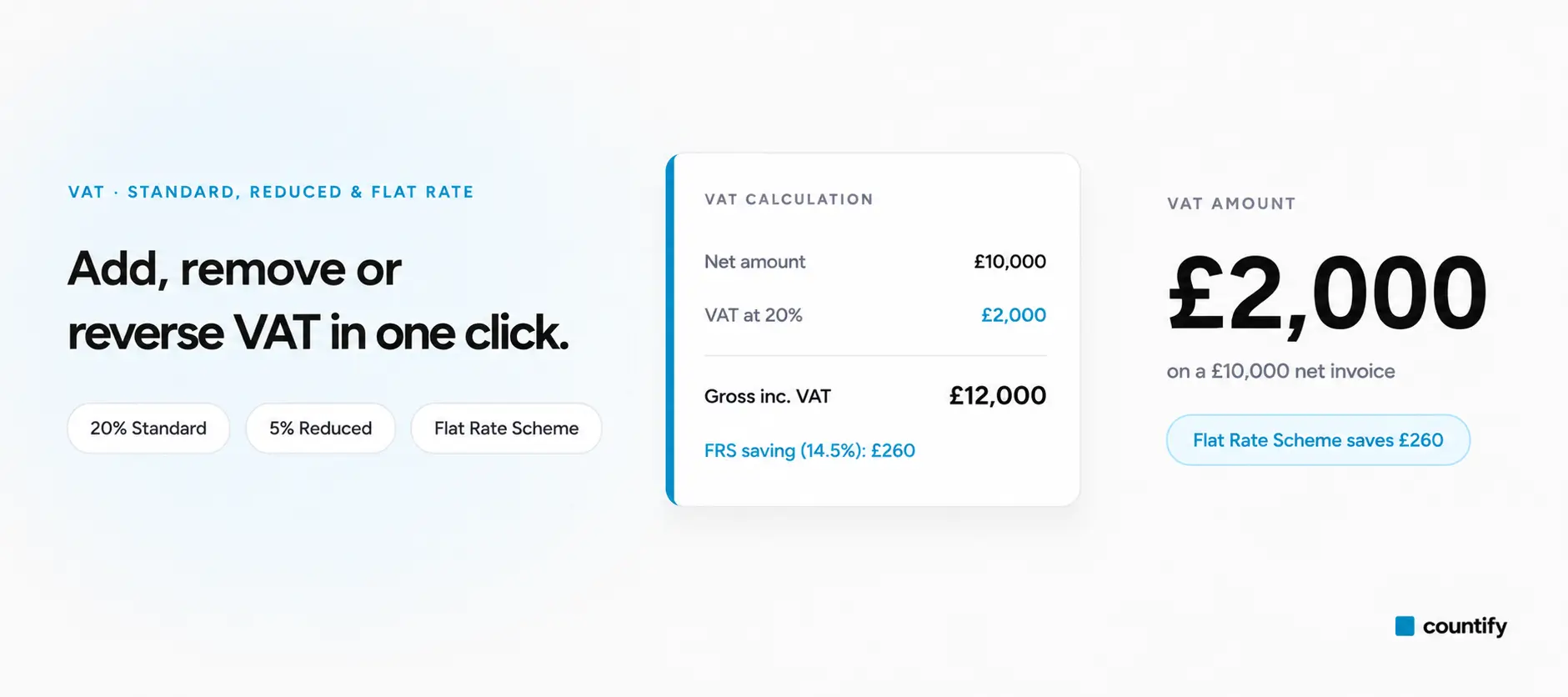

Calculate VAT from gross or net prices, switch between standard, reduced and zero rates, and model the Flat Rate Scheme used by many sole traders and small companies.

The UK VAT standard rate is 20%, with a reduced rate of 5% and a zero rate of 0%. To add VAT, multiply the net price by 1.20; to remove it from a gross figure, divide by 1.20. You must register for VAT once your taxable turnover exceeds £90,000 in any rolling 12-month period — the 2026/27 threshold — and register within 30 days of going over.

Gross (including VAT)

£1,200.00

at 20% VAT

VAT

£200.00

- Net

- £1,000.00

- VAT

- £200.00

- Gross

- £1,200.00

Are you better off on the FRS?

The Flat Rate Scheme lets you pay a fixed percentage of gross turnover instead of tracking input VAT line by line. Eligible if VAT-taxable turnover is under £150,000.

- Standard VAT

- £14,166.67

- FRS payable

- £12,325.00

- Annual difference

- £1,841.67 saved

Worked examples

VAT at the standard

20% rate.

The VAT added to common net prices at the UK 20% standard rate. Change the rate, amount or direction in the calculator above to model the reduced (5%) or zero (0%) rate, or to remove VAT from a gross total.

| Net price | VAT @ 20% | Gross price |

|---|---|---|

| £50.00 | £10.00 | £60.00 |

| £100.00 | £20.00 | £120.00 |

| £250.00 | £50.00 | £300.00 |

| £500.00 | £100.00 | £600.00 |

| £1,000.00 | £200.00 | £1,200.00 |

| £5,000.00 | £1,000.00 | £6,000.00 |

Figures use the 20% standard rate for the 2026/27 tax year. The reduced rate (5%) applies to items such as domestic fuel and children's car seats; the zero rate (0%) applies to most food, books and children's clothing.

Questions

Frequently asked

questions.

Multiply the net price by 1 plus the VAT rate. For the 20% standard rate, multiply by 1.2; for the 5% reduced rate, multiply by 1.05. The calculator does this automatically and shows the VAT element separately so you can copy it to your invoice.

Divide the gross figure by 1.20 (standard rate) or 1.05 (reduced rate). The remainder is the net price; the difference is the VAT element. The 'reverse VAT' direction in the calculator handles this automatically.

You must register for VAT once your taxable turnover exceeds £90,000 in any rolling 12-month period, or if you expect to exceed it in the next 30 days alone. You can also register voluntarily below the threshold to reclaim input VAT.

It depends on how much input VAT you would otherwise reclaim. The FRS is simpler and gives a 1% discount in the first year, but if you incur a lot of VATable expenses you may pay more under it. The comparison panel above shows your break-even at a glance — Countify can model this in detail.

Since April 2017, businesses on the Flat Rate Scheme whose goods cost less than 2% of turnover (or less than £1,000 a year) must use a fixed 16.5% rate, which effectively removes most of the FRS benefit. The category is common for consultancy and service businesses.

No. Domestic reverse charge (e.g. construction services under CIS) and cross-border B2B supplies require specific accounting entries. Get in touch with Countify if you need help structuring a reverse-charge invoice.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response