Self-Employed NI

Self-Employed NI Calculator (Class 2 & 4, 2026/27).

Calculate Class 2 and Class 4 National Insurance for sole traders and partners in 2026/27, including the £6,725 small-profits threshold and the 6% / 2% Class 4 rates.

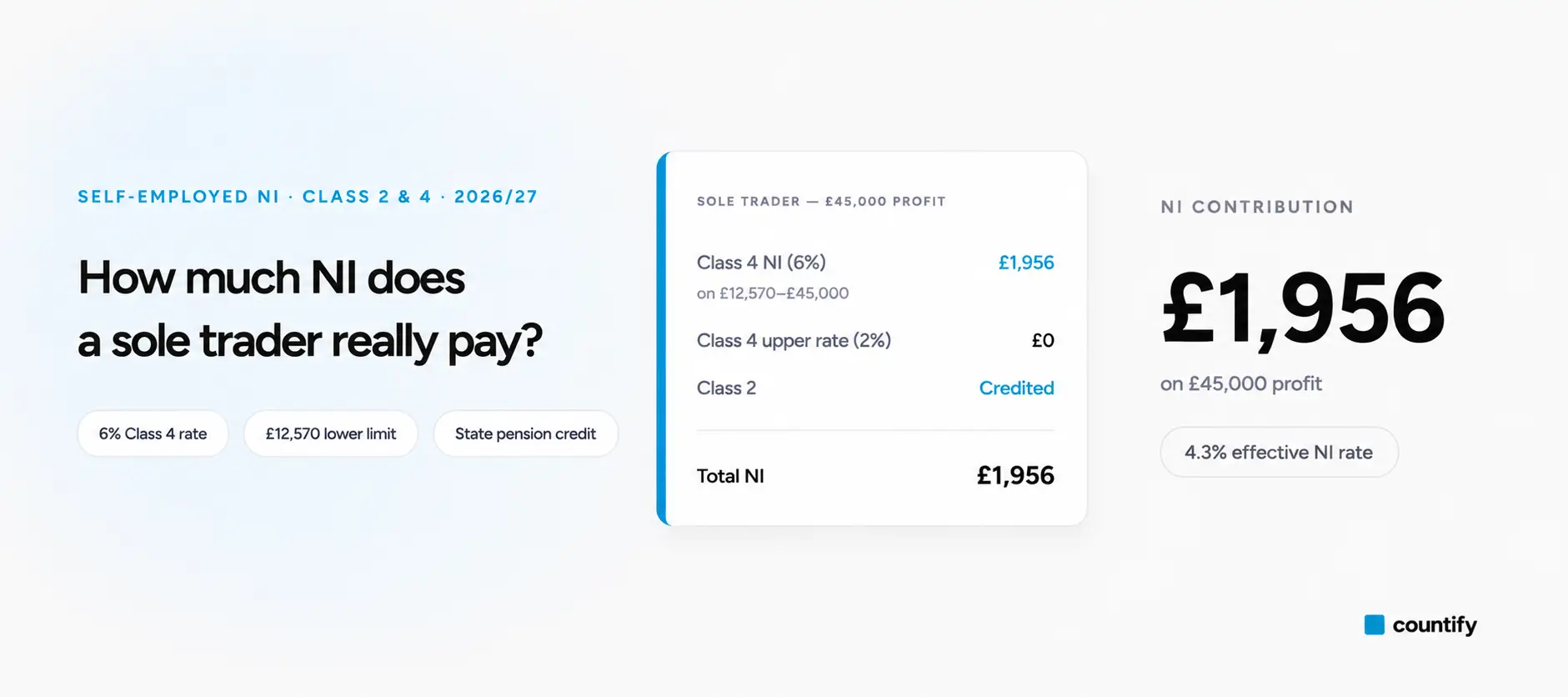

For 2026/27, self-employed Class 4 National Insurance is 6% on profits between £12,570 and £50,270, then 2% on profits above £50,270. Class 2 NI is no longer charged once profits reach the £6,725 small-profits threshold — you still receive the National Insurance credit toward your State Pension — but you can pay it voluntarily at £3.55 a week if your profits are below that level.

Total NI due

£1,526

Above £6,725 — you receive Class 2 credits automatically without paying Class 2.

- Class 2

- £0.00

- Class 4 main (6%)

- £1,525.80

- Class 4 upper (2%)

- £0.00

Questions

Frequently asked

questions.

Compulsory Class 2 was abolished from 6 April 2024 for sole traders earning above the £6,725 small-profits threshold. You still receive Class 2 contributions automatically (a credit) for state-pension purposes. Below the threshold, you can choose to pay voluntary Class 2 to keep your NI record complete.

Class 4 NI is 6% on profits between £12,570 and £50,270, and 2% on profits above £50,270. The 6% main rate is the result of a 2024 cut from 9%. Class 4 is calculated alongside your income tax through Self-Assessment.

Yes. Each partner pays Class 2 and Class 4 on their share of partnership profits, calculated as if they were a sole trader. The partnership return (SA800) reports the totals; each partner reports their share on SA100.

You need 35 qualifying years of NI to receive the full new state pension. Years are credited based on contributions or credits from being above the small-profits threshold. If you miss a year you can usually pay voluntary Class 2 retrospectively up to six years later.

No. National Insurance contributions are not an allowable expense against your trading profit. They are computed on your taxable profit figure and paid alongside income tax through Self-Assessment.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response