Dividends

UK Dividend Tax Calculator (2026/27).

Work out the personal tax on dividends for 2026/27 across the £500 dividend allowance and the 10.75%, 35.75% and 39.35% bands. Optimised for limited-company directors taking salary plus dividends.

For 2026/27 the first £500 of dividends is tax-free under the dividend allowance. Dividends above that are taxed at 10.75% in the basic-rate band, 35.75% in the higher-rate band and 39.35% in the additional-rate band. Dividends are treated as the top slice of your income, so your salary and other earnings decide which rate each pound of dividend is taxed at.

Take-home (post-tax)

£47,749

Total tax £4,821.25 · effective 9.2%

Dividend tax

£4,821.25

Dividend bands

- Dividend allowance (0%)£500.00

- Basic rate (10.75%)£37,200.00 → £3,999.00

- Higher rate (35.75%)£2,300.00 → £822.25

- Additional rate (39.35%)£0.00 → £0.00

- Income tax on salary£0.00

Worked examples

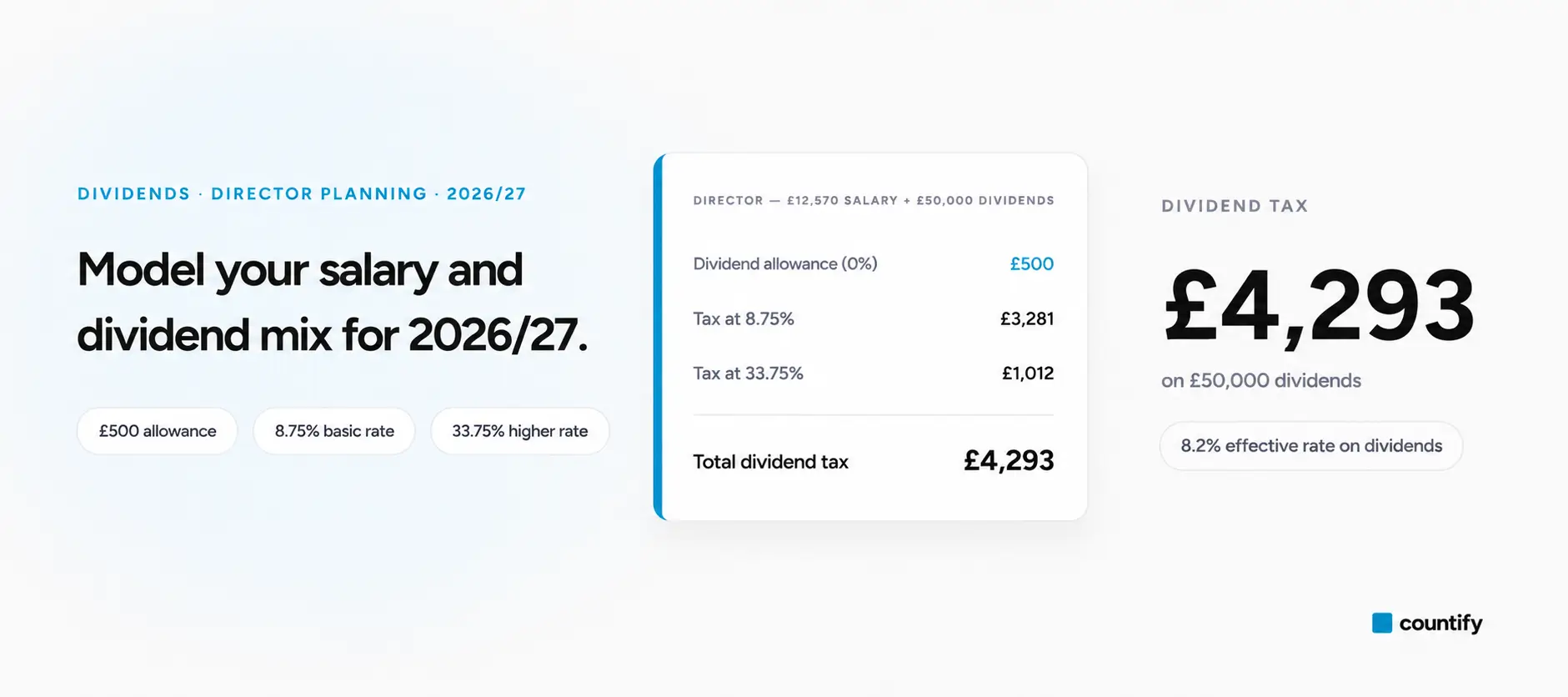

Dividend tax on a

director's draw.

The personal dividend tax due for 2026/27 on a director taking the typical £12,570 salary plus dividends on top. The first £500 of dividends is covered by the dividend allowance; the rest is taxed at 10.75% in the basic-rate band, then 35.75%.

| Dividends drawn | Dividend tax | Net in pocket |

|---|---|---|

| £10,000 | £1,021 | £8,979 |

| £20,000 | £2,096 | £17,904 |

| £30,000 | £3,171 | £26,829 |

| £40,000 | £4,821 | £35,179 |

| £50,000 | £8,396 | £41,604 |

Personal dividend tax only, on a £12,570 salary, for 2026/27. Figures exclude Corporation Tax already paid by the company and assume no other income — use the calculator above to model your own salary and dividend mix.

Questions

Frequently asked

questions.

Dividends above the £500 dividend allowance are taxed at 10.75% within the basic-rate band, 35.75% in the higher-rate band and 39.35% in the additional-rate band. The basic and higher rates each rose by 2 percentage points on 6 April 2026; the additional rate is unchanged.

The £12,570 personal allowance is used first against your total income, including dividends. Once it is exhausted, the £500 dividend allowance taxes the next slice of dividends at 0% — but those dividends still count toward your income-tax bands.

For 2026/27, a common structure is to take a salary up to the Class 1 Primary Threshold (£12,570) and the remainder as dividends. The salary preserves National Insurance credits, the dividends avoid employee and employer NI, and Corporation Tax relief is given on the salary cost. Countify can model this against your specific Corporation Tax position.

No. Dividend tax uses the UK-wide rates and bands; Scottish income-tax rates only apply to non-savings, non-dividend income such as salary and self-employed profit.

Dividend tax above the dividend allowance is settled through Self-Assessment. The balancing payment is due by 31 January following the tax year. If liabilities exceed £1,000, payments on account also apply.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response