IR35

IR35 Calculator: Inside vs Outside (2026/27).

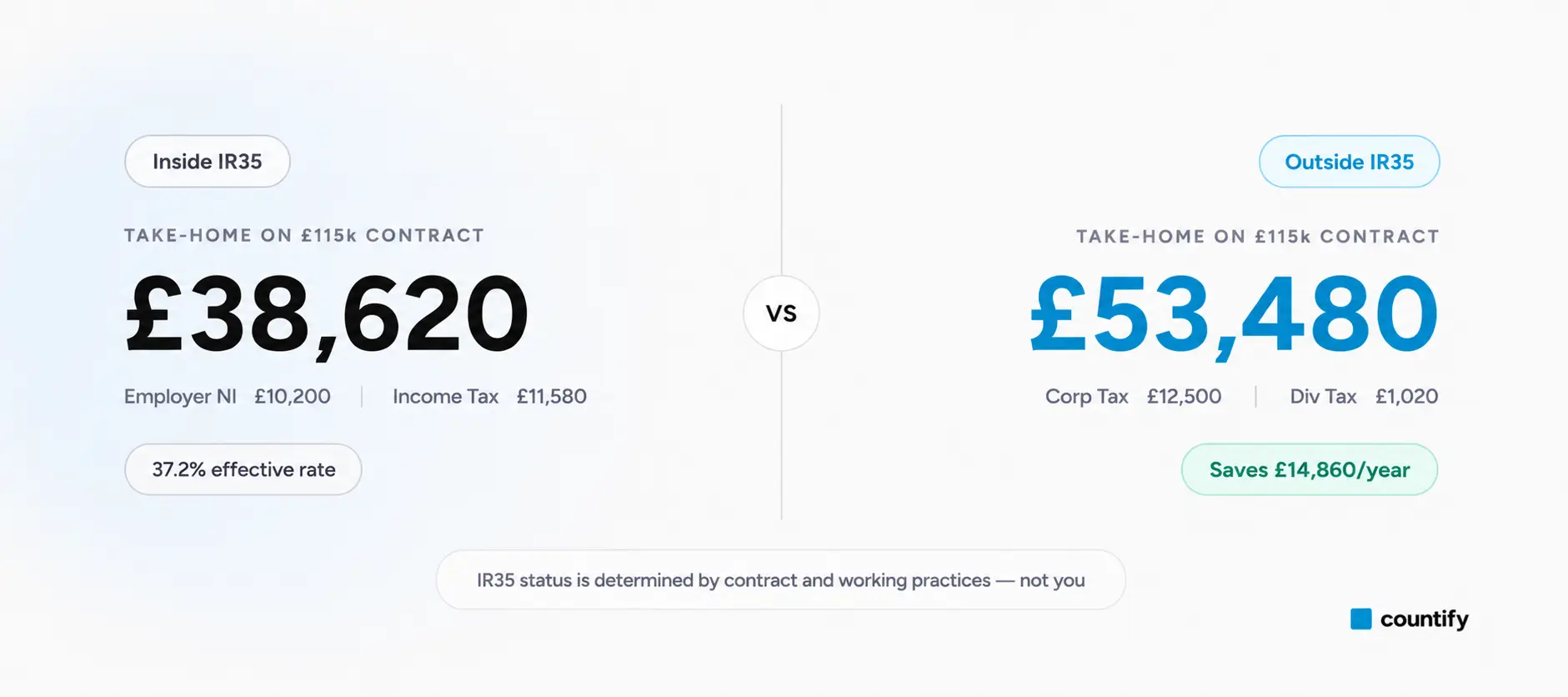

Compare your net take-home as a limited-company contractor inside IR35 versus outside IR35 for 2026/27, including salary plus dividends versus deemed-employment PAYE.

IR35 decides whether a contractor working through their own limited company is taxed like an employee. Outside IR35, you can take a small salary plus dividends, which is usually the most tax-efficient route. Inside IR35, the engagement is treated as deemed employment and taxed through PAYE with employee National Insurance, leaving less take-home. This calculator compares your net pay under both for 2026/27.

Annual contract value

£110,000

Outside IR35 advantage

£3,957/yr

Inside IR35 (deemed PAYE)

£65,222

Effective rate 40.7%

- Employer NI (15%)£15,750.00

- Income Tax£25,132.00

- Employee NI£3,895.60

Outside IR35 (Ltd · salary + dividends)

£69,179

Effective rate 37.1%

- Director's salary£5,000.00

- Corporation Tax£24,075.00

- Dividends after CT£80,925.00

- Dividend tax£16,745.66

Questions

Frequently asked

questions.

Inside IR35 means the engagement is treated as employment for tax purposes. The fee-payer (your agency or end client) deducts employer NI from the contract value first, then runs the remainder through PAYE — so you receive a net amount equivalent to an employee on the same gross salary, without any take-home benefit from operating through a limited company.

It depends on day rate and contract length, but for a £500 day rate across 220 working days, contracting outside IR35 with a low salary plus dividends typically nets around £8,000–£15,000 more per year than the inside-IR35 equivalent. The calculator above shows your exact figure.

For public-sector engagements and medium/large private-sector clients, the end client (or fee-payer) decides status and issues a Status Determination Statement (SDS). For small clients, the contractor's own limited company still decides. HMRC's CEST tool is the most common assessment route, though many advisers (Countify included) treat its output as guidance, not gospel.

Most travel and subsistence expenses are not deductible inside IR35 — the 'deemed employee' is treated as a permanent employee at the client's site for tax purposes. Outside IR35, a limited-company director can claim reasonable business expenses.

Not really. The status applies to the engagement as a whole. Different contracts with different clients can have different statuses, and Countify recommends a working-practices review for each new contract — particularly if you are mid-renewal.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response