Corporation Tax

UK Corporation Tax Calculator (2026/27).

Estimate UK Corporation Tax for the 2026/27 financial year, including marginal relief between the £50,000 small-profits threshold and the £250,000 main-rate threshold, with associated-company adjustments.

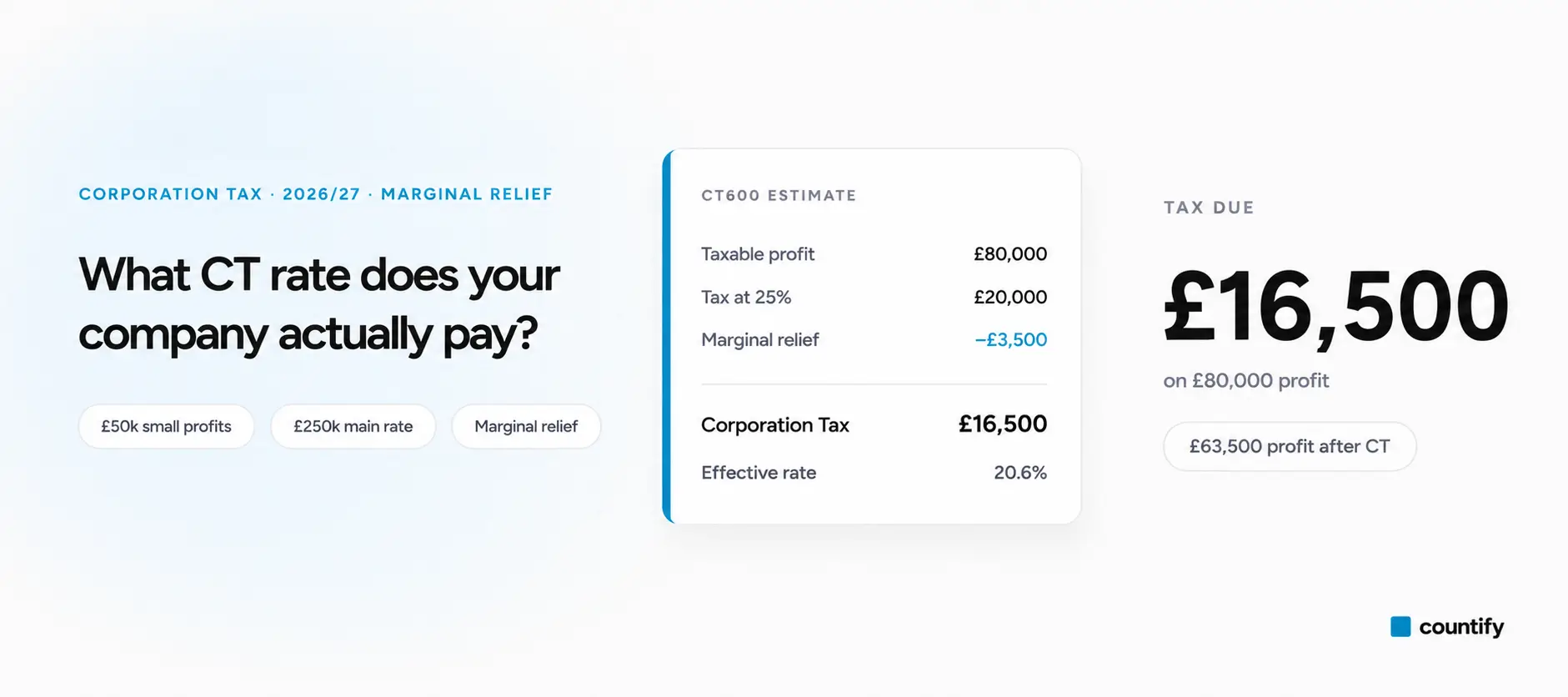

For the 2026/27 financial year, UK Corporation Tax is 19% on profits up to £50,000 (the small-profits rate) and 25% on profits of £250,000 or more (the main rate). Profits between £50,000 and £250,000 are charged at 25% with marginal relief, giving an effective rate of 26.5% on profits in that band. Both thresholds are shared between associated companies.

Corporation Tax due

£17,450

Marginal relief (25% less MR)

Effective rate

21.8%

- Profit after CT

- £62,550

- Lower threshold

- £50,000

- Upper threshold

- £250,000

Marginal relief breakdown

- Tax at 25% main rate£20,000.00

- Less marginal relief (3/200)−£2,550.00

- CT payable£17,450.00

Worked examples

Corporation Tax

across the bands.

The Corporation Tax due on common profit levels for the 2026/27 financial year, assuming one company with no associated companies. Notice the effective rate climb from 19% to 25% through the £50,000–£250,000 marginal-relief band.

| Taxable profit | Corporation Tax | Effective rate |

|---|---|---|

| £30,000 | £5,700 | 19% |

| £50,000 | £9,500 | 19% |

| £100,000 | £22,750 | 22.8% |

| £150,000 | £36,000 | 24% |

| £250,000 | £62,500 | 25% |

| £500,000 | £125,000 | 25% |

Estimates for the 2026/27 financial year. Associated companies, ring-fence profits and accounting periods that straddle 1 April are handled differently — use the calculator above, or speak to Countify.

Questions

Frequently asked

questions.

Companies with taxable profits up to £50,000 pay the small-profits rate of 19%. Above £250,000 the main rate of 25% applies. Between these thresholds the company is in the marginal-relief band — it pays 25% but receives a sliding-scale rebate using HMRC's 3/200 marginal-relief fraction.

Marginal relief is calculated as 3/200 × (£250,000 − augmented profits). This produces an effective tax rate between 19% and 26.5% as profits rise through the band. The calculator above shows the gross 25% charge and the marginal relief deduction separately.

Two companies are associated if one controls the other, or both are controlled by the same person or group of people. Associated companies share the £50,000 and £250,000 thresholds equally, which can push your company into the higher band sooner. The rules tightened from 1 April 2023 — Countify can review your group structure to confirm exposure.

Yes — Corporation Tax rates apply by financial year (FY) running 1 April to 31 March. An accounting period that straddles two financial years is apportioned. For an April-to-March year-end, FY 2026 covers the whole period and the rates above apply throughout.

The CT600 return is due 12 months after the end of the accounting period. The Corporation Tax payment is due earlier — 9 months and 1 day after the period end (or in quarterly instalments for very large companies). Use our deadline checker to confirm your exposure.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response