Stamp Duty

Stamp Duty, LBTT and LTT Calculator.

Estimate the property-purchase tax due in England and Northern Ireland (SDLT), Scotland (LBTT) and Wales (LTT). Supports first-time buyers and the additional-dwelling surcharge.

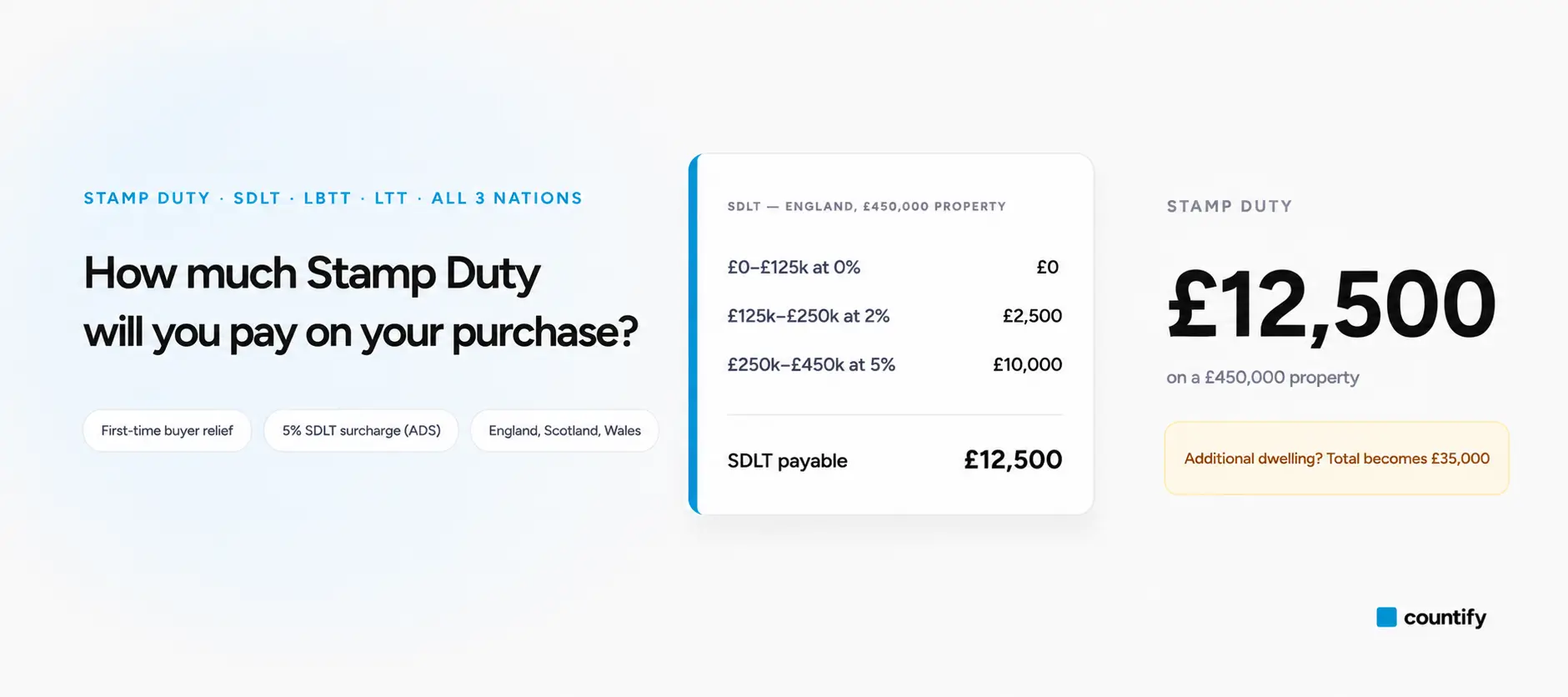

Property-purchase tax depends on the nation. In England and Northern Ireland, Stamp Duty Land Tax (SDLT) is 0% up to £125,000, 2% to £250,000 and 5% to £925,000. In Scotland, LBTT starts at 0% up to £145,000; in Wales, LTT starts at 0% up to £225,000. First-time-buyer relief and the additional-dwelling surcharge change these rates — the calculator applies the correct bands for your nation and buyer type.

SDLT payable

£5,000

Effective rate 1.7% on £300,000

Band-by-band breakdown

- £0 – £125,000 at 0%£125,000.00 → £0.00

- £125,000 – £250,000 at 2%£125,000.00 → £2,500.00

- £250,000 – £925,000 at 5%£50,000.00 → £2,500.00

Questions

Frequently asked

questions.

From 1 April 2025 the residential SDLT bands reverted to pre-COVID levels: 0% to £125,000, 2% to £250,000, 5% to £925,000, 10% to £1.5m, and 12% above. First-time buyers pay 0% up to £300,000 and 5% on the slice between £300,000 and £500,000, with no relief if the price exceeds £500,000.

LBTT residential bands for 2026/27 are 0% to £145,000, 2% to £250,000, 5% to £325,000, 10% to £750,000 and 12% above. First-time buyers pay 0% up to £175,000. The Additional Dwelling Supplement (ADS) is 8% on second homes and buy-to-let purchases since 5 December 2024.

Wales has no first-time buyer relief but a higher 0% threshold of £225,000. The next slice to £400,000 is 6%, then 7.5% to £750,000, 10% to £1.5m and 12% above. Additional-dwelling LTT starts at 5% from the first pound and rises through six bands.

SDLT returns and payment in England and Northern Ireland are due within 14 days of completion. LBTT (Scotland) and LTT (Wales) are due within 30 days. Returns are filed by your conveyancer, who deducts the duty from completion funds.

Yes. Limited companies pay HRAD / ADS on residential property regardless of the number of dwellings owned. From £500,000, companies acquiring single residential dwellings also fall within the 17% flat SDLT charge unless a relief (e.g. property rental business) applies.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response