Structure comparison

Sole Trader vs Limited Company: Tax Comparison (2026/27).

Compare take-home pay as a sole trader versus an optimally structured limited company director for 2026/27, including income tax, Class 4 NI, Corporation Tax and dividend tax.

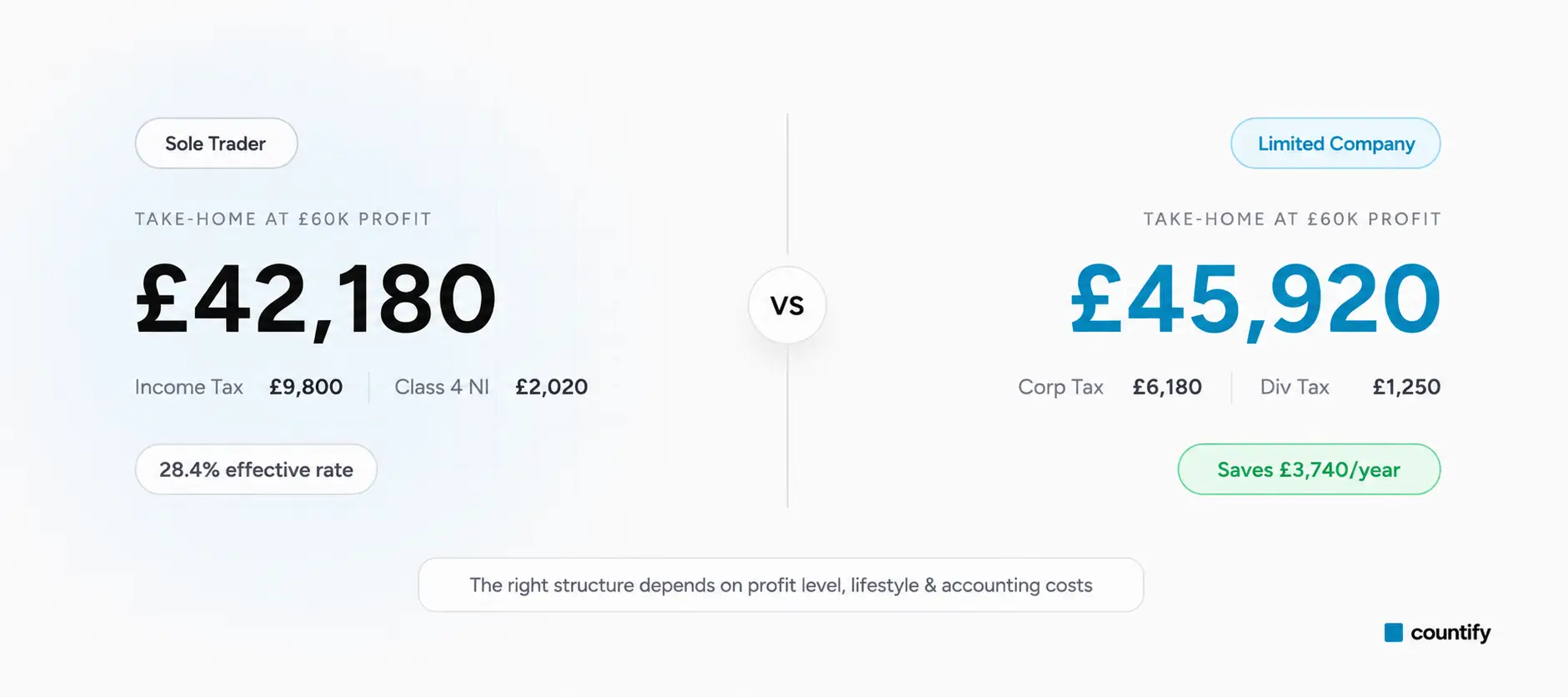

As a sole trader, all your profit is taxed through Self-Assessment at Income Tax rates plus Class 4 National Insurance. As a limited company director, profit is taxed first at Corporation Tax (19%–25%), and you then extract it as a small salary plus dividends, usually paying less overall once profits are higher. This calculator compares take-home pay under both structures for 2026/27 so you can see the crossover point.

Sole trader

Take-home

£46,111

Effective rate

23.1%

- Income Tax

- £11,432.00

- Class 4 NI

- £2,456.60

- Total tax

- £13,888.60

- Take-home

- £46,111.40

Limited company (optimal)

Take-home

£46,091

Effective rate

23.2%

- Director salary

- £12,570.00

- Employer NI

- £1,135.50

- Corporation Tax

- £8,795.96

- Dividend Tax

- £3,977.34

- Total tax

- £13,908.80

- Take-home

- £46,091.20

The limited company structure costs £20.20 more per year at this profit level.

This comparison uses the optimal salary + dividends structure for a sole director. Actual savings depend on your business expenses, pension contributions, family shareholding and other factors. Countify can model your exact situation.

Source: gov.uk Corporation Tax rates. Rates for the 2026/27 tax year.

Related calculators

Keep planning.

Employer NI

Employer PAYE Calculator

True cost of employment: employer NI at 15%, auto-enrolment pension, monthly breakdown.

Corporation Tax

Corporation Tax Estimator

Estimate CT600 with marginal relief between £50k and £250k profit.

Dividends

Dividend Tax Calculator

Salary + dividends modelled for limited-company directors, with the £500 allowance.

Questions

Frequently asked

questions.

No. It depends on the profit level, how much cash you need personally and the extra admin costs. A limited company often becomes advantageous around £30,000 to £35,000 of profit once accounting costs are factored in.

A salary of £12,570 sits at the personal allowance and the employee NI primary threshold, so there is no income tax and no employee National Insurance. A small employer NI charge of around £1,135 still applies above the £5,000 secondary threshold for sole-director companies that cannot claim Employment Allowance.

No. You should usually add £1,000 to £2,500 per year for limited company accounts, depending on complexity and the level of support needed.

Yes, with proper structuring. The arrangement must be commercially and legally sound, and Countify can advise on settlement legislation and the correct share structure.

It typically makes sense when profit consistently exceeds £35,000 to £40,000 and you do not need to extract all profit personally each year.

Get started

Take control of your

numbers today.

Free, no-obligation consultation. We agree the fee upfront — no surprises.

- Expert advice

- Fixed fees

- Fast response